A fintech COO closing out a Series B round doesn’t have a talent problem. She has a sequencing problem. KYC volumes are climbing 20% a quarter, the board wants operating costs down without touching the product roadmap, and every offshoring conversation she’s had this year has pitched the same thing regardless of what stage the company is actually in — a fully staffed team, a long contract, and a sales rep who disappears the moment the ink dries.

The mistake isn’t offshoring. It’s picking a model built for a company three stages ahead of — or behind — where the fintech actually sits. A 40-person lending startup validating its onboarding flow doesn’t need a legal entity in India. A regulated payments company processing millions of transactions a month can’t run compliance-critical functions on a staffing subscription. The model has to match the stage, not the other way around.

This is the decision most fintech operators actually face: virtual staffing, managed teams, Build-Operate-Transfer, or a full Global Capability Center. Each one is a legitimate way to build offshore capability. None of them is universally correct. Here’s how to match the model to where your fintech actually stands.

Why the Model Choice Matters More in Fintech

Fintech isn’t logistics or e-commerce. Every offshore function — KYC document review, transaction monitoring, chargeback handling, loan servicing — touches money movement, customer financial data, or a regulatory obligation. That changes the calculus in three ways:

Compliance ownership has to be explicit. When an AML alert gets missed or a reconciliation break goes unnoticed, “the vendor was responsible for that” isn’t an answer regulators or auditors accept. Whoever owns the process needs to own the control environment around it.

Volume is not linear. Transaction volume, application volume, and support ticket volume swing hard with funding cycles, product launches, and market conditions. A model that’s efficient at one volume can be badly mismatched six months later.

Cost per transaction is the metric that matters, not headcount cost. A cheaper analyst who takes twice as long to clear a KYC case isn’t actually cheaper. The right model has to improve throughput and accuracy, not just lower a line item on the P&L.

Get the model wrong and you either overpay for infrastructure you don’t need yet, or you run regulated processes on a staffing arrangement that was never designed to carry that weight. This is exactly the tension OwnGCC’s fintech GCC solutions are built around — matching KYC, AML, payments, and lending operations to a model that can actually carry them.

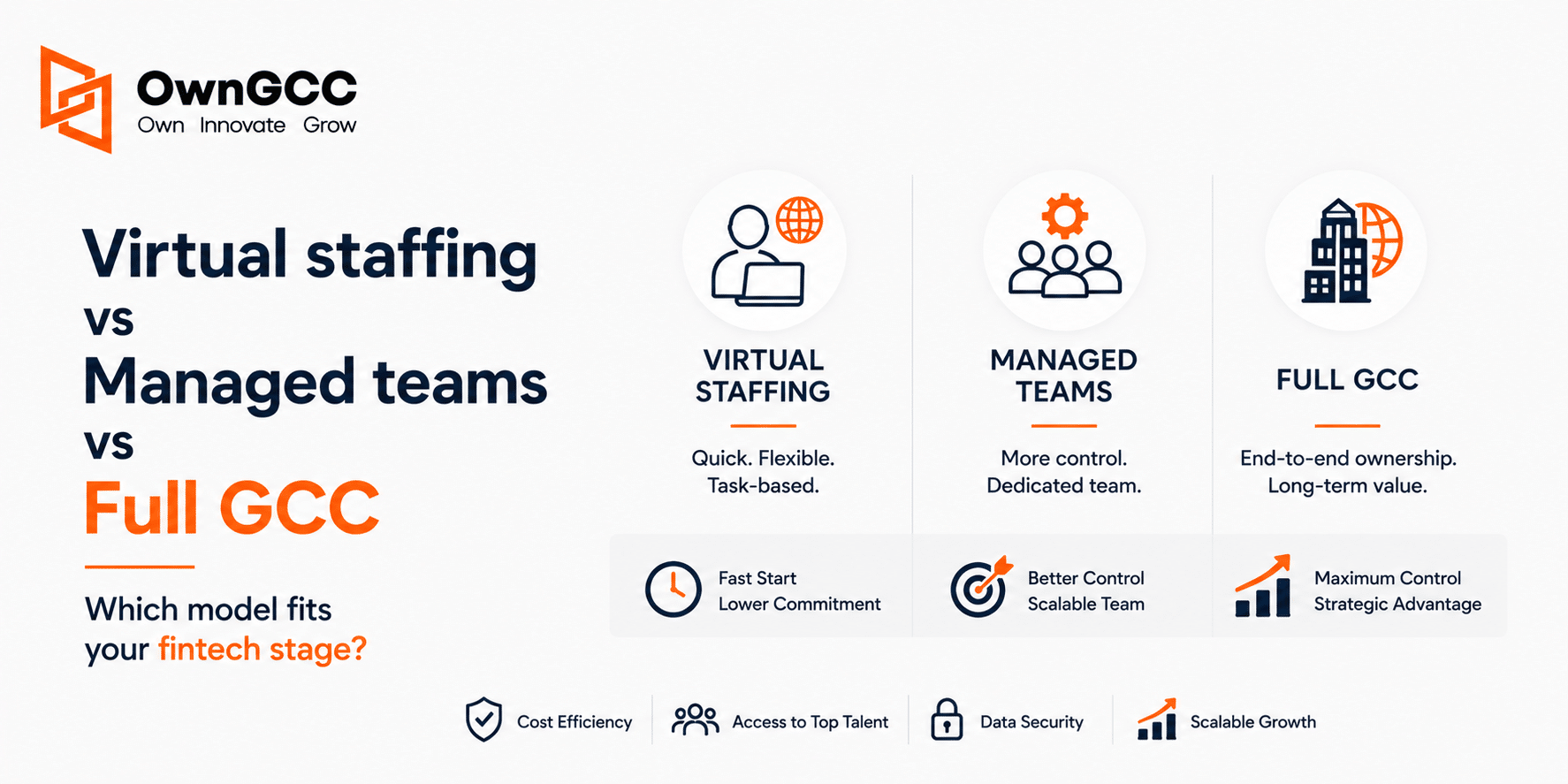

The Four Models, Mapped to Fintech Maturity

Virtual Staffing — For Fintechs Validating Before They Scale

What it is: You define the role, and OwnGCC sources, screens, and hires the person. Once onboarded, that analyst works under your direct management — you own training, workflows, and performance. OwnGCC stays in the background as the hiring and continuity partner, stepping back in only if a replacement is needed.

Where it fits: Early-stage and scale-up fintechs — post-seed through Series A — that need role-specific expertise (a KYC analyst, a reconciliation specialist, a support lead) without committing to team-level infrastructure. It’s also the right entry point for a fintech that isn’t sure offshoring is right for them yet and wants to test it on one or two roles before making a bigger commitment.

What you get: Zero lock-in, full management control, and a fast way to add capacity around a single function like onboarding review or L1 support. What you don’t get is a managed operating layer — SOPs, QA, infrastructure, and process governance are yours to build.

Fintech read: Good for a lending startup adding its third underwriting support analyst, or a payments company that needs one dedicated chargeback specialist while its internal ops lead is still defining the process. Not the right model for a compliance function that needs standardized QA and audit trails from day one — that oversight is on you to build, and in fintech that’s a heavier lift than it looks.

Managed Teams — For Fintechs Scaling Operations, Not Just Headcount

What it is: OwnGCC manages hiring, payroll, compliance, workspace, and IT for a full-time distributed team, while operations run against your workflows and SLAs. It goes beyond staffing — you get an integrated team with HR, legal, finance, and infrastructure support built in, without carrying that overhead internally.

Where it fits: Growth-stage fintechs — typically Series B and beyond — that have moved past validating individual roles and now need a functioning team: a KYC/AML pod, a payments operations desk, a loan servicing unit. Volume is real, SLAs matter, and the operational lift of managing HR, compliance, and infrastructure for an offshore team in-house isn’t worth building yet.

What you get: Faster team-building, integrated support across HR and compliance, and cost savings without the burden of standing up your own entity. What you’re trading is some direct control — OwnGCC is handling more of the operational scaffolding around the team than in virtual staffing.

Fintech read: This is where most of OwnGCC’s fintech engagements for KYC/AML checks, transaction monitoring support, payment reconciliation, and MIS reporting land. It’s built for the stage where a fintech needs a real operational bench, not just headcount, but isn’t ready to own the entity, workspace, and compliance infrastructure outright.

Build-Operate-Transfer — For Fintechs That Know They’ll Own This Eventually

What it is: OwnGCC stands up a dedicated legal entity for your team, hires “GCC-ready” talent aligned to your compensation and culture, and operates the center under a structured playbook — designed from day one to be handed over. Unlike a staffing arrangement, the team, IP, and processes are built as if they were already yours; ownership is a transfer of an existing structure, not a rebuild.

Where it fits: Late-stage growth or pre-IPO fintechs that have already proven the offshore model works through managed teams and now want a captive center — but don’t want the capital outlay, hiring risk, and 12-18 month setup time of building one from scratch. This is the model for a fintech that has decided ownership is the destination and just needs a de-risked way to get there.

Fintech read: Fits a fintech scaling its risk, compliance, and financial crime function into a standing team of 30-100+ people, where the regulatory and continuity stakes are high enough that “eventually we’ll own this” needs to become a concrete transition plan with a legal entity already in place — not a someday conversation.

Full GCC — For Regulated, Scale-Stage Fintechs That Need Full Control Now

What it is: OwnGCC’s GCC-as-a-Service model gives you a fully operational, wholly-owned capability center — legal entity, workspace, IT infrastructure, talent, and governance — built out through a subscription model rather than heavy upfront capital investment. You own the center; OwnGCC handles the setup and operational scaffolding.

Where it fits: Mature or highly regulated fintechs — public companies, late-stage unicorns, or fintechs operating under heavier supervisory scrutiny — that need full operational control over compliance, financial crime, and core processing functions from day one. At this stage, “we’ll transition to ownership later” isn’t good enough; auditors, regulators, and the board expect direct oversight now.

Fintech read: This is the model for a fintech running its own risk and compliance organization end-to-end, with regulatory reporting, audit trails, and financial crime operations sitting inside a center it directly controls — not a shared or transitional arrangement.

Comparing the Four Models

| Dimension | Virtual Staffing | Managed Teams | BOT | Full GCC |

|---|---|---|---|---|

| Fintech Stage | Seed – Series A | Series B – Growth | Late Growth / Pre-IPO | Mature / Regulated Enterprise |

| Control | Full (You manage) | Shared | High, transitioning to full | Full from day one |

| Compliance Ownership | Built by your team | Process & QA support included | Structured transition to your organization | Fully in-house |

| Speed to Launch | Fastest (single roles) | A few weeks | Longer (entity setup) | Several weeks, no capex |

| Cost Structure | Subscription per role | Bundled per team | Investment toward future ownership | Subscription that scales with the center |

| Best For | Testing offshore operations | Building an operations function | Preparing for full ownership | Maximum regulatory control |

| Natural Next Step | → Managed Teams | → BOT or Full GCC | → Full GCC | Owned & continuously optimized |

How to Decide: A Stage-Based Framework

Three questions cut through most of the indecision:

How regulated is the function you’re moving offshore? Product support and back-office data entry tolerate more flexibility than KYC/AML, transaction monitoring, or regulatory reporting. The more compliance-critical the function, the more it needs the process rigor of managed teams or above — not a staffing arrangement carrying that weight alone.

What’s your volume trajectory over the next 12 months? If volume is still unpredictable, virtual staffing or managed teams keep you flexible. If you’re forecasting sustained, high-confidence growth — the kind that justifies a standing team of 50+ — BOT or full GCC start paying for themselves.

Is ownership the destination, or is flexibility? Some fintechs want to own their offshore operation outright, permanently. Others want offshore capability without the entity, workspace, and governance overhead. There’s no wrong answer, but the honest one determines whether you start with BOT (ownership is the plan) or managed teams (flexibility is the point).

The Models Aren’t a Ladder You’re Forced to Climb

None of this locks you in. A fintech can start with virtual staffing to hire its first offshore KYC analyst, move to managed teams once volume justifies a full pod, and evaluate BOT once the function is core enough to own outright — or it can walk in at managed teams or full GCC on day one if the stage and regulatory profile already call for it. The point isn’t to sell every fintech on the most complex model. It’s to match the engagement to where the operation actually is, and leave a clear path to the next stage when it’s earned, not forced.

FAQs

Can we switch engagement models without disrupting operations?

Yes — the transition between models is designed to be structural, not a rebuild. Moving from virtual staffing to managed teams, for example, adds process governance and infrastructure around an existing team rather than replacing it. BOT is explicitly built to transfer an already-operating team and entity, not to start over.

Who owns compliance risk under each model?

Under virtual staffing, you own compliance process design and oversight — OwnGCC handles hiring and continuity. Under managed teams, process, QA, and audit trail structure are built in alongside the team. Under BOT and full GCC, compliance infrastructure is designed to sit inside your own governance from the outset, with full GCC giving you direct, unshared control.

How long does it take to move from managed teams to BOT?

It depends on team size and the complexity of the functions involved, but because BOT is designed to be transfer-ready from setup, the transition is a structured handover against an existing legal entity and operating playbook — not a new build. Timelines are typically scoped during the discovery and strategic blueprint phase before the engagement starts.

Is a full GCC worth it for a fintech that isn’t public yet?

Not usually. Full GCC makes the most financial and operational sense once regulatory scrutiny, transaction volume, and headcount needs are large enough to justify direct, full-time ownership of the infrastructure. Most fintechs get more value from managed teams or BOT until they hit that scale — full GCC without the volume to support it just means paying for capacity you don’t need yet.

Does virtual staffing work for compliance-critical roles like KYC or AML?

It can for a single, well-defined role — but the process rigor, QA, and audit trail structure around that role are yours to build under virtual staffing. Most fintechs move compliance-critical functions to managed teams once volume grows, specifically because that structure comes built in.