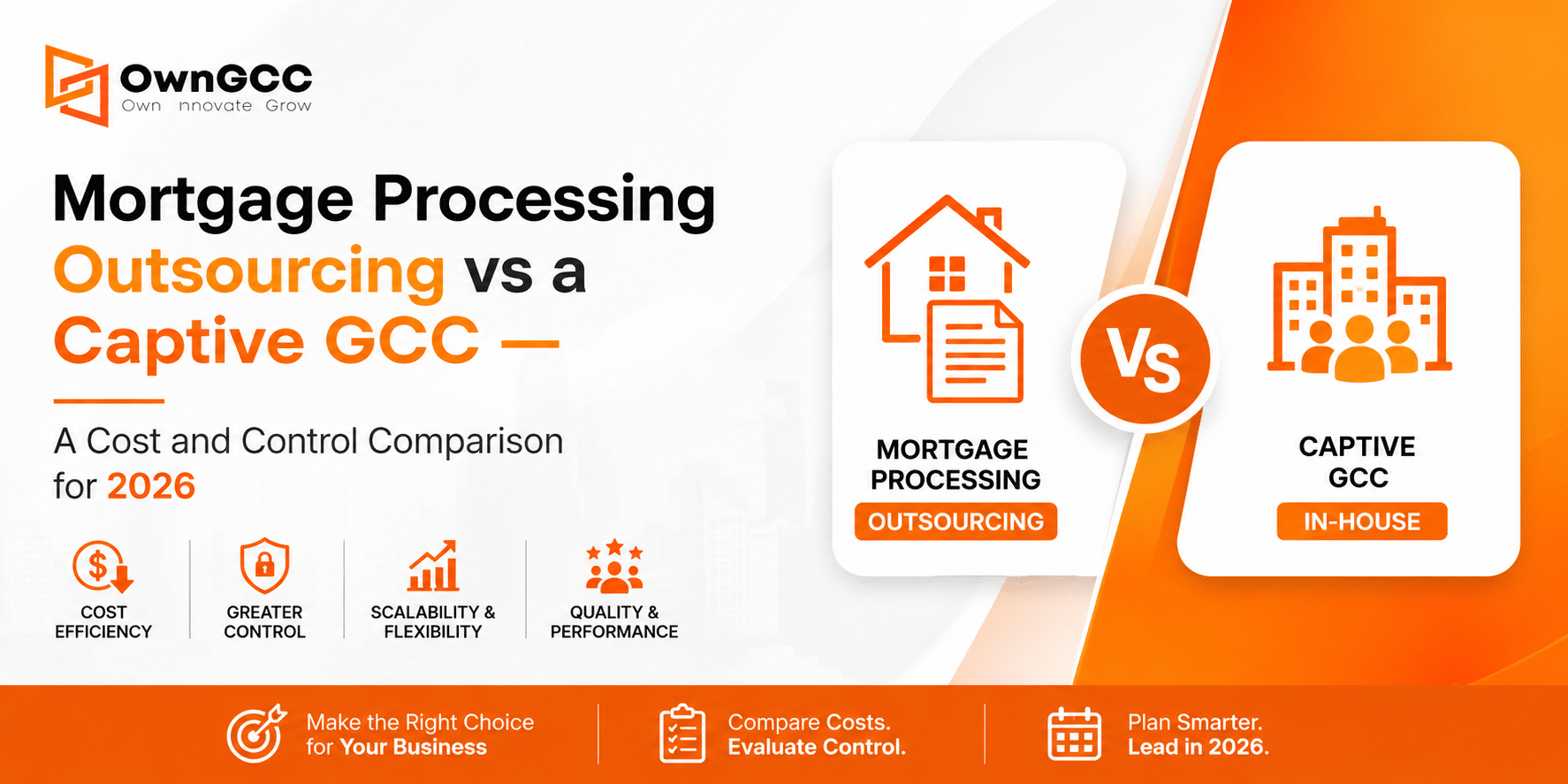

Mortgage processing outsourcing has long been the default answer for lenders looking to cut costs and manage volume. But in 2026, a growing number of mortgage firms are asking a harder question: what if we built our own offshore team instead?

This comparison breaks down the real costs, control trade-offs, and compliance implications — so you can make the right call before renewing your next outsourcing contract.

Outsourcing gives you speed and low setup costs. A captive GCC gives you control, IP ownership, and significantly lower per-unit costs at scale. For firms processing 300+ loans per month, the GCC almost always wins on a 3-year ROI basis.

Why Mortgage Firms Are Rethinking Outsourcing

Third-party outsourcing providers offer a simple pitch: send the loan files, pay per file, skip the headaches. And for years, that worked. But the hidden costs of mortgage processing outsourcing are becoming harder to ignore:

- Cost inflation at scale: Per-unit pricing scales linearly — you pay more as volume grows, with no economies of scale.

- Data exposure risk: Borrower PII sits on a shared vendor infrastructure, raising CFPB and state-level compliance concerns.

- No IP retention: Workflow improvements your team develops with a vendor belong to the vendor — not you.

- Vendor lock-in: Switching vendors or bringing operations in-house is expensive and disruptive.

- Limited customization: Vendors optimize for efficiency across clients, not for your specific loan products or guidelines.

What Is a Captive GCC in Mortgage?

A Captive Global Capability Center (GCC) is your own offshore team — a wholly-owned subsidiary, not a vendor relationship. The people, processes, data, and IP all belong to your firm.

India has become the dominant location for mortgage GCCs, offering a large pool of English-speaking finance professionals, competitive salary structures (typically 60–70% below US equivalents), and a mature regulatory framework for foreign subsidiaries.

Head-to-Head: Mortgage Processing Outsourcing vs Captive GCC

| Dimension | Outsourcing (TPO) | Captive GCC (India) |

|---|---|---|

| Setup Cost | Low — vendor absorbs | $500K–$1M (Year 1) |

| Ongoing Cost | Higher per-unit pricing | 30–50% lower at scale |

| Data Control | Shared infrastructure | Private, dedicated environment |

| IP Ownership | Vendor retains process IP | 100% yours |

| Customization | Limited / packaged | Unlimited |

| Compliance Control | Vendor’s SLAs govern | Your internal controls |

| Talent Alignment | Pooled resources | Hired to your standards |

| Break-even Timeline | Immediate | 12–18 months post-setup |

The Cost Math: When Does a GCC Win?

At 500 loans per month, a typical outsourcing vendor charges $150–$250 per file — roughly $75,000–$125,000 monthly. A captive GCC of 25–30 FTEs in India, fully loaded, runs $40,000–$60,000 per month by Year 2. That’s a potential saving of $420,000–$780,000 annually — flowing directly to your bottom line.

Firms processing 300+ loans per month typically reach GCC break-even within 12–18 months. Below 200 loans/month, outsourcing or a hybrid model usually makes more sense.

Control, Compliance & IP — The Strategic Case

- Regulatory compliance: With a GCC, you own the compliance framework — your policies, your audits, your data governance. No dependency on a vendor’s controls.

- IP and process innovation: Every workflow improvement stays inside your firm and compounds over time as institutional knowledge.

- Talent alignment: Your GCC team is trained to your loan products, underwriting guidelines, and quality standards — structurally impossible in a pooled-resource model.

- Business continuity: No single-point-of-failure from vendor instability, M&A activity, or contract disputes.

When Outsourcing Still Makes Sense

To be clear — outsourcing isn’t always the wrong answer. It remains appropriate when:

- Monthly volume is below 200–250 loans and GCC setup economics don’t yet apply

- Your firm is in an uncertain growth phase and needs volume flexibility

- Internal management bandwidth is limited for the first-year GCC ramp

- You need a bridge solution while your captive center stands up

Frequently Asked Questions

In Year 1, yes — outsourcing has lower setup costs. From Year 2 onward, a captive GCC in India is typically 40–55% more cost-efficient for firms processing 300+ loans per month. The advantage grows with volume.

With ownGCC’s structured model, most mortgage lenders achieve full operational ramp within 9–12 months. First team members are typically onboarded within 3–4 months of kickoff.

Virtually every back-office and middle-office function: loan setup, document verification, processing, underwriting support, QC, compliance, title coordination, closing, post-closing, and servicing. GCCs are not limited to commoditized tasks.

Typically safer than in a third-party outsourcing model. Because the GCC is wholly-owned, you control data governance, access controls, encryption, and audit trails — borrower PII stays within your corporate infrastructure.

Yes — and this is often the recommended approach. Running both in parallel during the ramp phase maintains volume continuity while you build internal capability. Most clients transition volume gradually over 6–9 months.